Contenido multimedia no disponible por derechos de autor o por acceso restringido. Contacte con la institución para más información.

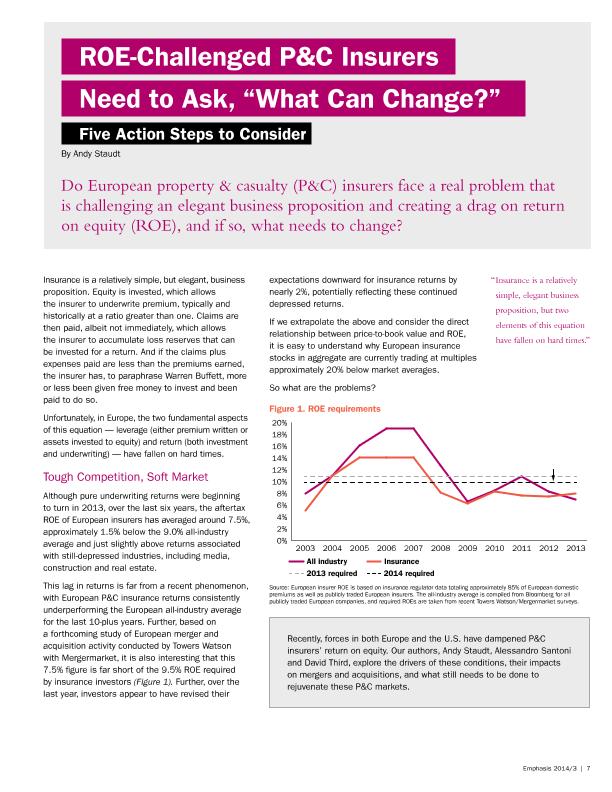

MAP20140040360Staudt, AndyROE-challenged P&C insurers need to ask, "What can change?" : five action steps to consider / Andy Staudt Sumario: Although pure underwriting returns were beginning to turn in 2013, over the last six years, the aftertax ROE of European insurers has averaged around 7.5%, approximately 1.5% below the 9.0% all- ndustry average and just slightly above returns associated with still-depressed industries, including media, construction and real estate.This lag in returns is far from a recent phenomenon, with European P&C insurance returns consistently underperforming the European all-industry average for the last 10-plus years. Further, based on a forthcoming study of European merger and acquisition activity conducted by Towers Watson with Mergermarket, it is also interesting that this 7.5% figure is far short of the 9.5% ROE required by insurance investors (Figure 1). Further, over the last year, investors appear to have revised their expectations downward for insurance returns by nearly 2%, potentially reflecting these continued depressed returns. If we extrapolate the above and consider the direct relationship between price-to-book value and ROE, it is easy to understand why European insurance stocks in aggregate are currently trading at multiples approximately 20% below market averagesEn: Emphasis. - New York : Towers Watson, 1987-. - 30/10/2014 Número 3 - 2014 , p. 7-101. Seguro de daños patrimoniales. 2. Inversiones. 3. Rendimiento. 4. ROE. 5. Rentabilidad. 6. Recursos propios. 7. Empresas de seguros. 8. Europa. I. Title.