Contenido multimedia no disponible por derechos de autor o por acceso restringido. Contacte con la institución para más información.

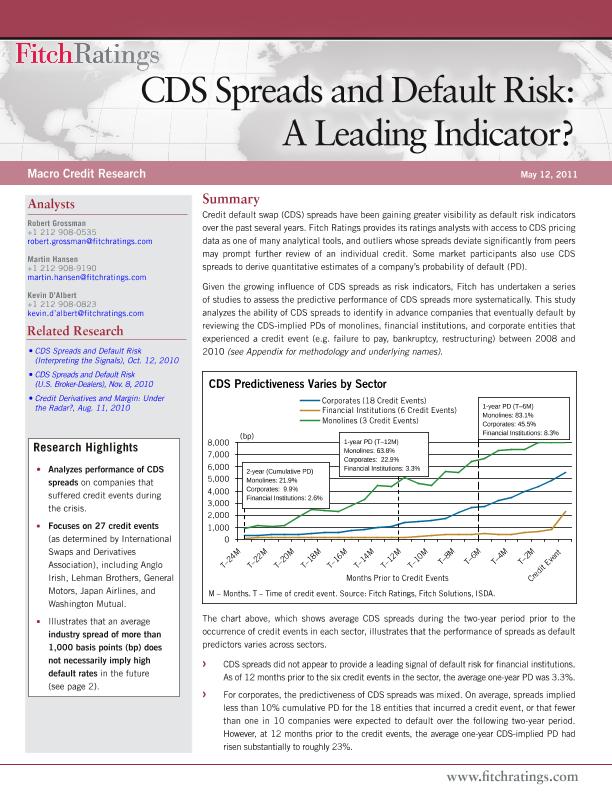

Seção: Documentos eletrônicosTítulo: CDS spreads and default risk : a leading indicator? / Robert Grossman, Martin Hansen, Kevin DAlbertAutor: Grossman, RobertPublicação: New York : Fitch Ratings, 2011Notas: Sumario: Credit default swap (CDS) spreads have been gaining greater visibility as default risk indicators over the past several years. Fitch Ratings provides its ratings analysts with access to CDS pricing data as one of many analytical tools, and outliers whose spreads deviate significantly from peers may prompt further review of an individual credit. Some market participants also use CDS spreads to derive quantitative estimates of a company's probability of default (PD)Materia / lugar / evento: Riesgo crediticioInstrumentos financierosIncumplimiento de pagoSeguro de créditoOtros autores: Hansen, Martin D'Albert, Kevin Fitch Ratings Outras classificações: 327.1Direitos: In Copyright (InC)